The memory chip industry is entering a new stage of accelerated price rise and substantial profit expansion-the latest research report of Nomura Securities shows that the price increase in the third quarter will far exceed previous expectations, and the profit gap between HBM and general DRAM will be gradually bridged around 2027.

According to the news of Chasing Wind Trading Desk, Nomura Securities released a global storage industry research report on June 24th, raising the target price of SK Hynix by 18% from 4 million won to 4.7 million won, maintainingSamsung ElectronicsPrice Target 670,000 KRW(It was previously raised from 590,000 won on June 22)。 As of the date of release of the report,Samsung ElectronicsThe share price was 340,500 won, representing an implied upside of 96.8%; SK Hynix shares traded at 2.58 million won, representing an implied upside of 82.2%.

There are two core driving forces for the target price increase: First, the increase in storage price in the third quarter greatly exceeded previous expectations; Second, Nomura simultaneously raised its 2027 earnings forecast and made more moderate assumptions about the magnitude of the won appreciation.

Price increases in the third quarter greatly exceeded expectations

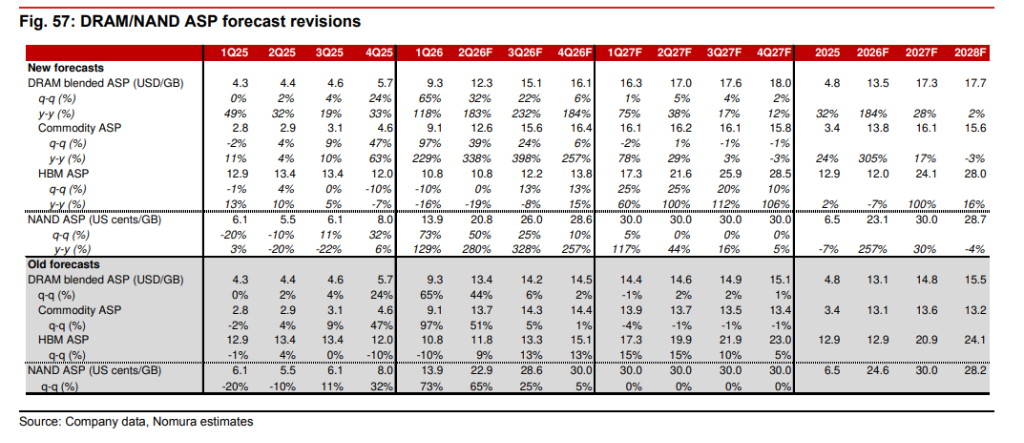

The bank had previously forecast a quarter-over-quarter increase in general purpose DRAM prices of about +5% and NAND of about +25% in the third quarter. The latest report raised the DRAM gain forecast directly to +24% QoM, and NAND remained unchanged at +25% QoM.

There are three clues in the logic of price increase to advance at the same time.

First, the price increase of consumer products (mobile phones, PCs, etc.) in the second quarter was relatively moderate, forming a low base, and there was more room for compensatory increase in the third quarter. Second, the purchase prices of DDR5 and LPDDR5 by cloud service providers (CSPs) continued to rise. Third, the proportion of HBM4 products with higher unit prices in the sales structure has increased, raising the overall average selling price (ASP).

Analysts also expect that the growth rate of shipments in the second half of the year will exceed that in the first half of the year, as the contribution of new capacity will be gradually released over time.

Profit differentiation in the second quarter:SamsungExceeding expectations, Hynix's operating profit is slightly lower but net profit is bright

In the second quarter, the profit trends of the two companies showed obvious differentiation.

Samsung ElectronicsOn the other hand, analysts raised their second-quarter operating profit forecast to 76 trillion won from 67 trillion won in the June 15 report.The main reason is that the labor agreement finalized the bonus payment ratio of 10.5%, lower than the previous assumption of 12%, and the corresponding bonus provision dropped from 24 trillion won to 19 trillion won.At the same time, it is pointed out that the price increase achieved by Samsung in the second quarter is "in line with the previous assumptions as a whole" and is larger than that of its peers.

However, Samsung's non-storage business is under obvious pressure. The handset business (MX segment) has fallen into the red in the hardware business due to rising memory costs. Analysts estimate that although Samsung has raised the price of smartphones by 10%-15%, it is still not enough to fully cover the impact of rising memory costs. Foundry/LSI business losses were also widened by higher bonus expenses.

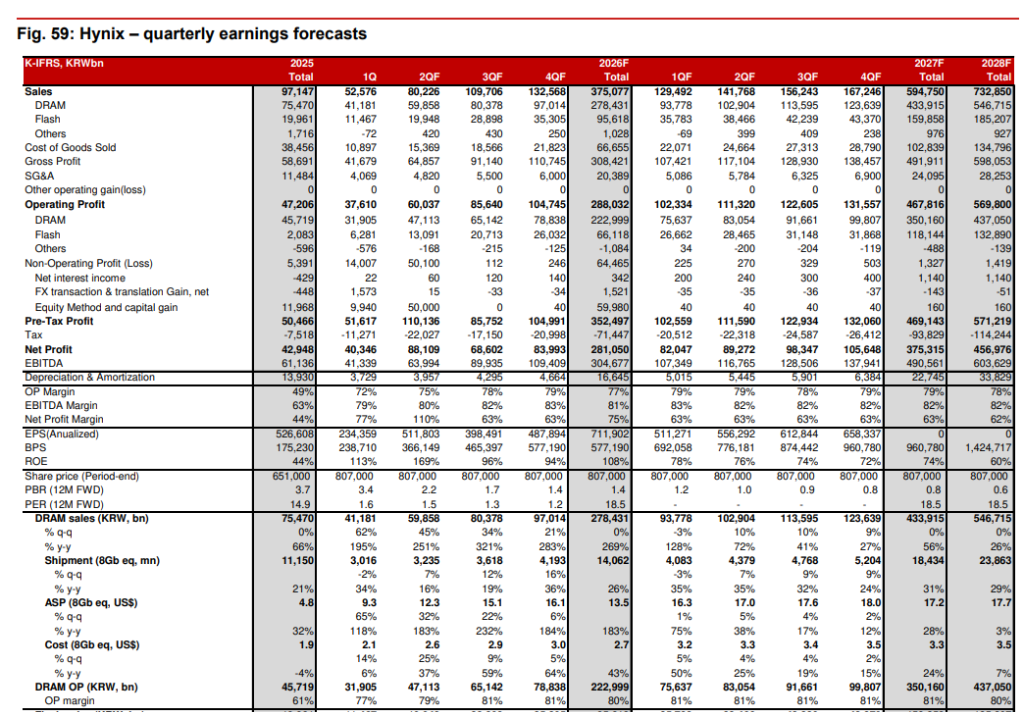

SK HynixOn the other hand, analysts expect its operating profit in the second quarter to be about 60 trillion won, slightly lower than previous expectations. The reason is that the price increase of consumer electronics and smartphone-related products temporarily lagged behind server products in the second quarter, which was more than expected.

But Hynix's net income will significantly beat market expectations.Analysts estimate that the valuation gain of Kioxia convertible bonds (about 14% equity) held by Hynix in the second quarter will be about 54 trillion won, and the combined non-operating income related to Kioxia will exceed 60 trillion won together with the gain from the disposal of the remaining SPC1 equity.Therefore, it is expected that Hynix's net profit in the second quarter will be close to 100 trillion won.

Analysts pointed out that Hynix's initial investment in Kioxia was about 4 trillion won, and the total return so far is estimated to be 70 trillion to 80 trillion won, with a return multiple of nearly 20 times.

HBM Profitability: Way Below General DRAM Currently, On Track to Tied in 2027

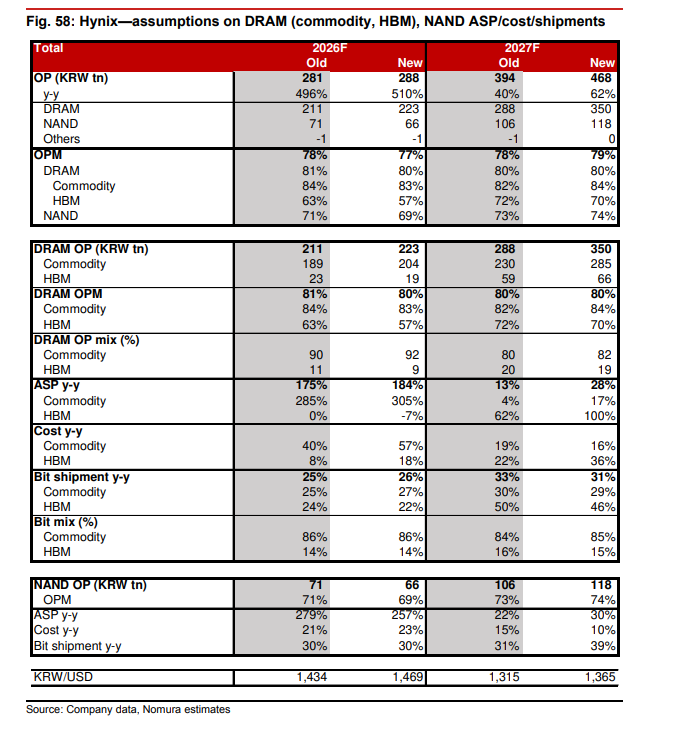

Nomura noted that HBM's current operating margin (OPM) is about 50%, while that of general purpose DRAM is about 80%. There is a huge gap between the two.

The line illustrates the difficulty of tying with a simple mathematical logic:For HBM products to achieve profitability levels similar to those of general DRAM, the selling price needs to increase by more than 100%.This means that HBM has much more room and necessity for price increases than general DRAM.

Because of this, the bank believes that the price increase of HBM in 2027 is "increasingly likely to exceed previous expectations" and raised the HBM pricing assumptions accordingly. In SK Hynix's forecast model, HBM's ASP is expected to significantly lift from approximately $12/GB (1Gb equivalent) in 2026 to approximately $24.1/GB in 2027, an increase of approximately 100%.

Forecasts for SK Hynix show that HBM's operating margin will improve from approximately 57% in 2026 to approximately 70% in 2027, gradually moving closer to approximately 84% of general purpose DRAM.

Long-term agreement negotiations ongoing, terms vary from supplier to customer

The long-term supply agreements (LTAs) are expected to be mainly with cloud service providers (CSPs) andNVIDIASign.

It is understood that each storage supplier is currently in LTA negotiations with about 2 to 4 customers, with negotiation progress and key terms, including pricing and advance payments, varying from supplier to customer.

Analysts expect the LTA to be enforced from the second half of 2026 or 2027, when visibility of the relevant provisions will improve. The specific terms of the LTA have not been disclosed, but its impact on the profitability of each supplier may diverge.

Samsung's Dividend may increase nearly 9 times as its 2027 earnings forecast is sharply raised

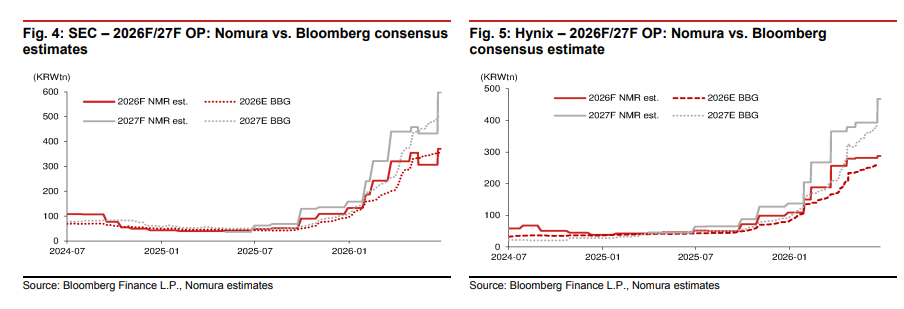

The bank raised its operating profit forecast for Samsung Electronics in 2026 and 2027 to 37.1 trillion won and 59.8 trillion won, respectively (up 21% and 38% from its May 15 forecast, respectively). SK Hynix's 2027 operating profit forecast was raised by 19% to 46.8 trillion won from 39.4 trillion won.

Two drivers of the upward adjustment: First, the increase in storage price is higher than previously assumed; Second, Nomura's forecast of the appreciation of the Korean won is more moderate-he believes that the overseas mergers and acquisitions of Korean enterprises and the overseas asset allocation demand of domestic institutional investors will be significantly greater than the historical law in this storage super cycle, thus restraining the excessive appreciation of the Korean won.

In terms of shareholder returns, Nomura expects that Samsung Electronics will start share repurchases from the second half of the year for employee compensation and shareholder returns, and some of the repurchased shares may be cancelled. Assuming a 25% Dividend payout ratio is maintained, the total Dividend will reach about 97 trillion won in 2027, an increase of about 9 times from 2025, corresponding to a yield of about 4.5% on common shares in Dividend and about 7.5% in preferred shares (both based on current share prices).

Four major risks cannot be ignored

The report also lists four risks that require ongoing attention.

First, the risk of delay in data center construction.If there are significant delays in U.S. data centers due to labor shortages, insufficient power supply or social resistance, AI hardware supply chain demand will be negatively affected.

Second, AI market concentration risk.If the competitive landscape of AI developers evolves into a highly concentrated market structure, the bargaining power of AI hardware supply chain may weaken. The bank believes this stage has not been reached yet, but signs of market concentration could emerge as early as 2027 to 2029.

Third, the risk of production expansion by Chinese storage manufacturers.It is estimated that Chinese storage suppliers currently account for approximately 30% of China's domestic storage market share and close to 10% of the global market share. If Chinese manufacturers accelerate production expansion through localization of semiconductor equipment, it may have an impact on the bulk storage market.

Fourth, the capital flow risk after the stock price rises sharply.Shares of Samsung and Hynix have risen seven to 20 times from their 2025 lows, and both are already more than 10% weighted in emerging markets benchmark funds. Korea National Pension's domestic equity allocation has also exceeded its ceiling, meaning there could be selling pressure as shares rise further. Supply and demand dynamics are expected to improve from the second half as both companies accelerate their share buybacks and cancellations.

Comments