Even Netanyahu (Isreali PM) cannot bring Cisco more business?? What a non-sense and ridiculous war!

$Cisco(CSCO)$ announced its FY24Q1 results, with the stock price plummeting 12%. Although the quarterly performance was still good, it lowered its full-year guidance for the 24th fiscal year.

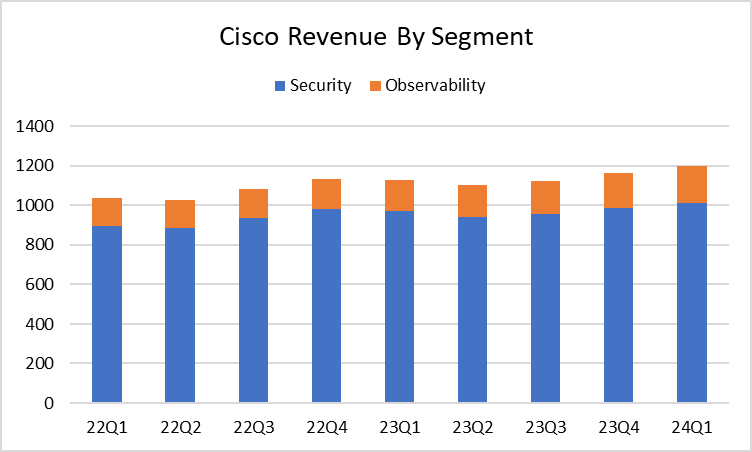

In the quarter (FY24Q1), CSCO achieved revenue of $14.67 billion, with market expectations of $14.63 billion, of which service revenue was $3.53 billion and product revenue was $11.14 billion.

The adjusted gross margin was 67.1%, and EPS was $1.11, higher than the market expectation of $1.03. The remaining performance obligations were $34.8 billion.

FY24Q2 guidance: revenue is expected to be between $12.6 billion and $12.8 billion, far below the market expectation of $14.2 billion. The adjusted gross margin is expected to be between 65% and 66%, lower than the consensus of 65.6%.

FY2024 guidance: It is expected that the annual sales in 2024 will be between $53.8 billion and $55 billion, lower than the previous expectation of $57 billion to $58.2 billion, due to the slowdown in new orders. The market consensus for annual sales is $57.84 billion. The expected EPS for fiscal year 2024 is between $3.87 and $3.93, lower than the estimated $4.05 per share.

The company stated that the main reason for the slowdown may be that customers are focusing on installing and implementing products after strong product delivery in three quarters. After customers implement a large number of recently shipped products, it is expected that the growth rate of product orders will accelerate in the second half of the year.

One sentence: Although not directly stated, Cisco’s demand has slowed down.

Comments