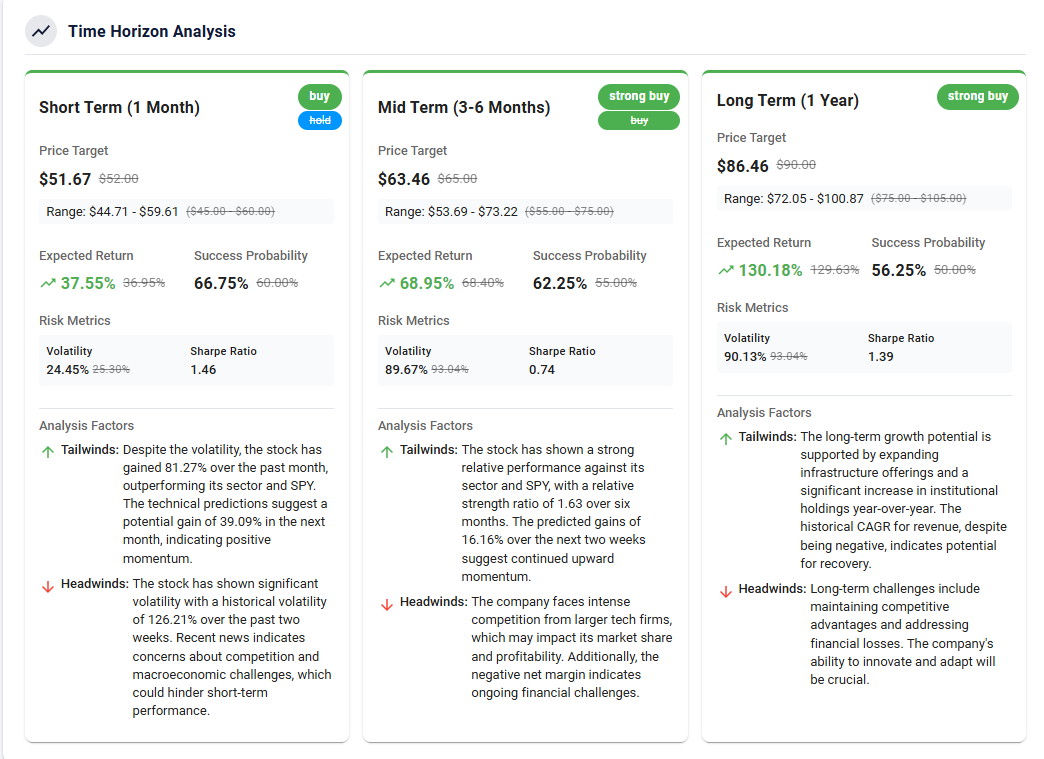

$NEBIUS(NBIS)$ 25Q1 earnings were strong overall (both revenue and ARR) thanks to rapid expansion of core AI infrastructure business and deepening NVIDIA partnership, though losses due to high capex remain a near-term pressure.Strategic investment in Toloka and optimistic outlook for full-year ARR guidance provide catalysts for valuation re-pricing, but competitive pressuresand governance risks require close attention.

The progress of data center go-live and improved profitability will be key variables in the coming quarters and could drive the market to reassess Nebius' positioning in the AI infrastructure space.

Performance and market feedback

1. Core financial metrics vs. market expectations

Revenue: Nebius Q1 2025 revenue came in at $55.3M, up 385% YoY, showing strong growth momentum, primarily driven by the core AI infrastructure business.However, revenues were slightly below market expectations (Zacks Consensus Estimate of $57.73M).

Earnings Per Share (EPS): reported EPS of -$0.39, better than the market's estimate of -$0.45, indicating that the company exceeded expectations in terms of cost control or operational efficiency.

Adjusted EBITDA: Adjusted EBITDA loss was $62.6M, better than market expectation of -$94.4M, indicating that the company's loss was lower than expected along with high growth, reflecting some operational leverage.

Annualized revenue (ARR): March ARR reached $249M, far exceeding the market's expectation of $220M and up 684% YoY, indicating strong revenue growth potential. April ARR further increased to ~$310M, up 24.5% YoY, highlighting the rapid expansion of the business.

2. Share price performance and market sentiment

After-hours performance: Nebius shares rose ~1.1% after-hours following the earnings release, reflecting the market's positive reaction to the above-expectation EPS and ARR performance, despite slightly lower-than-expected revenues.

INVESTOR SENTIMENT: The market's optimism on Nebius stems largely from the rapid growth of its AI infrastructure business and the reaffirmation of its $750M-$1B annual ARR guidance.However, revenue misses and continued losses have triggered caution among some investors, and the stock has been under pressure recently (down 19.5% over the past three months, underperforming the tech sector).

Investment highlights

AI infrastructure business drives strong growth, ARR a key metric

Nebius Q1 2025 revenue growth of 385% YoY with core AI Infrastructure business being the key driver highlighting the company's rapid penetration in the global AI infrastructure market.Annualized Run Rate Revenue (ARR) reached $249M, a significant increase from $90M in Dec 2024, and ARR further increased to ~$310M (+24.5% MoM) in April, demonstrating strong customer demand for the Nebius AI Cloud Platform.

The ARR outperformance demonstrates the company's progress in acquiring long-term contracts and customer stickiness, especially against the backdrop of surging demand for AI workloads such as training and inference.Nebius has strengthened its competitiveness in the high-performance computing market by deploying Hopper and Blackwell GPU clusters through its partnership with NVIDIA.However, the lower-than-expected revenues may reflect the fact that new data centers (e.g., Kansas City and Paris) are not yet fully online, and that revenue recognition is lagging the rapid growth of ARR.

Rapid ARR growth is a core trigger for valuation repricing.The market is likely to link Nebius' ARR growth to a revenue multiple, which is expected to be in the range of $525M-$613M in 2025, validating the company's full-year $520.5M revenue guidance.If Nebius continues to meet its ARR targets ($750M-$1B by year-end), its valuation could see further upside, especially driven by a high growth premium in the AI infrastructure space.

Short-term pressure from high capex & infrastructure expansion

Up to $808.1M in capex in 2024, primarily for GPU clusters and datacenter build-outs in the U.S. (Kansas City, NJ) and Europe (Finland, France, Iceland) In Q1 2025, a 5MW datacenter is expected to go live in Kansas City by the end of the quarter, with plans to deploy thousands of NVIDIA Hopper GPUs and to expand to 40MW; a Finnish datacenterplanned to expand to 75MW by the end of 2025.

In addition, the Company announced that it will deploy over 22,000 NVIDIA Blackwell GPUs by 2025, further strengthening its position in the high-end AI computing market.However, high capex resulted in adjusted EBITDA loss of -$62.6M and net loss of -$113.6M, reflecting the company's earnings pressure during its rapid expansion phase.

High capex is a major source of short-term earnings pressure, but is also a necessary investment for long-term growth.The market is likely to remain wary of continued losses and cash flow pressures, especially against giants such as Amazon AWS and Microsoft Azure, where Nebius is smaller and still in the early stages of market share expansion.However, successful go-live of new data centers and GPU clusters will significantly improve revenue recognition and may gradually ease loss pressure in Q2-Q3 2025.

Toloka Strategic Investment and Business Diversification

On May 7, 2025, Nebius announced that its AI data solutions business, Toloka, received a $72M strategic investment led by Bezos Expeditions with participation from Shopify CTO Mikhail Parakhin, increasing Toloka's autonomy and bringing in external professional management.Toloka's 2024Toloka's revenue growth of 140% YoY in 2024 and the addition of several leading global base model producer customers in Q4 demonstrates strong demand in the generative AI data market.

This investment not only provides Toloka with expansion capital, but also boosts market confidence through its association with a prominent investor.However, Nebius retains a majority stake but relinquishes voting control, potentially raising investor concerns about corporate governance.

Toloka's strategic investment could provide a positive catalyst for Nebius' overall valuation, especially against the backdrop of continued demand for generative AI data.However, the ceding of voting control may lead to market concerns about the consistency of future strategic decisions, and subsequent governance restructuring needs to be closely monitored.

Management Guidance and Market Expectations

Nebius reiterated full year 2025 ARR guidance of $750M-$1B, demonstrating management's continued confidence in AI infrastructure demand.The company expects 2025 revenues to be in the range of $500M-$600M, which is slightly ahead of market expectations of $520.53M. management highlighted in the earnings call that the go-live of the Kansas City and Finland datacenters, as well as the deployment of Blackwell GPUs, will significantly drive revenue growth.However, guidance does not provide a clear path to profitability, and the market may have reservations about the sustainability of continued losses and high capital expenditures.

The reaffirmation of guidance reinforces the market's confidence in Nebius' growth prospects, but the uncertainty over the earnings path could limit the valuation premium.Investors need to watch Q2 for further validation of ARR growth and acceleration of revenue recognition.

Market Competition and Risk Factors

Nebius faces stiff competition in the AI cloud infrastructure market from giants such as Amazon, Microsoft, and Google, which have captured more than half of the global cloud infrastructure market.Nebius has gained differentiation by focusing on AI-specific workloads and partnering with NVIDIA, but it is small and infrastructure expansion still takes time.The stock has underperformed over the past three months (-19.5%), reflecting market concerns about its competitive position and profitability.In addition, the dual shareholding structure (founder Arkady Volozh holds a majority of voting rights) could raise governance concerns and affect long-term investor confidence.

Competitive pressures and governance structure may limit short-term valuation upside, but deeper cooperation with NVIDIA and innovative platforms such as AI Studio may win Nebius niche market share and support valuation repricing in the long term.

Comments