Domino's Q3 Earnings Explosion: Supply Chain Saves the Day, But Stores Struggle!

$达美乐比萨(DPZ)$ released its third-quarter financial results for fiscal year 2025 on October 14. Overall, the company continued to grow revenue driven by promotions, product innovation, and channel expansion. However, profitability faced slight pressure on net income due to rising costs and fluctuations in non-operating items. Specifically:

We break down each operational metric and its underlying logic in detail.

Key Investment Considerations

Revenue growth continues to be driven positively, maintaining steady expansion, supported by both supply chain and royalty fee performance.

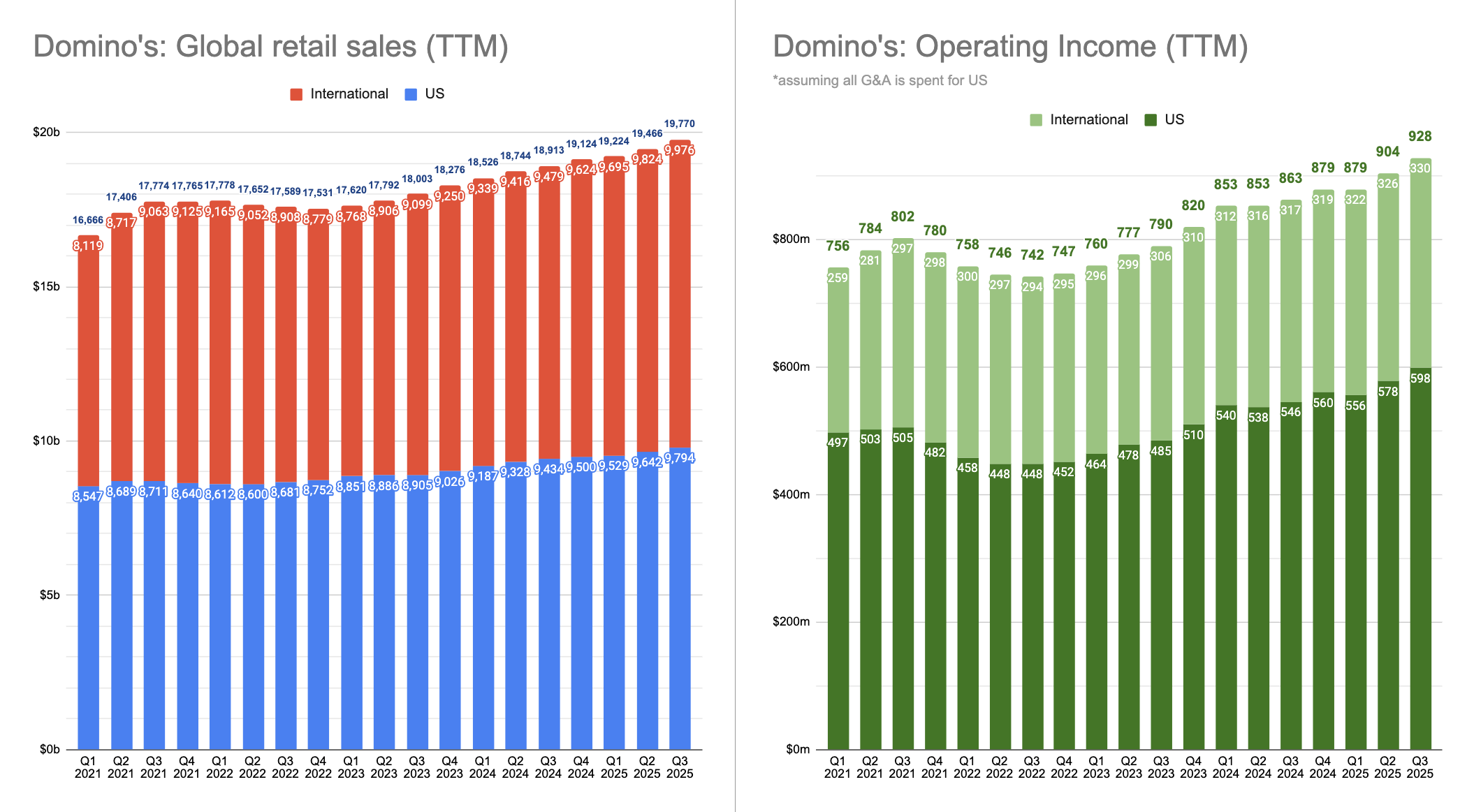

Total revenue reached $1.1471 billion, a 6.2% year-over-year increase, surpassing the average analyst estimate of $1.139 billion. Key drivers included increased supply chain revenue ($697 million) and higher U.S. franchise fees ($157.2 million), reflecting the pull effect of promotions like "Best Deal Ever" and Parmesan Stuffed Crust. This metric demonstrates the effectiveness of the company's pricing and mix strategies in the U.S. market, while the continued strengthening of the supply chain's share in the business structure (approximately 60%) reinforces its role as an ecosystem platform.

Within supply chain revenue, food basket pricing contributed to a store markup increase of approximately +3.3% (year-over-year).

Although commodity costs have risen, procurement productivity has partially offset this impact, leading to an improvement in supply chain gross margin (up 0.7 percentage points year-on-year).

Against a backdrop of less-than-optimistic macroeconomic conditions, the company has managed to drive steady revenue growth by leveraging supply chain markups and channel leverage, reflecting its resilience in pricing power and operational efficiency. However, ongoing monitoring of cost risks—including rising prices for raw materials, transportation, and labor—will be essential moving forward.

Directly operated stores face gross profit pressure, with overall gross profit margins showing signs of divergence. Supply chain operations have seen a slight improvement in gross profit margins.

Gross profit margins at company-owned stores in the U.S. declined by 0.5 percentage points year-over-year, primarily driven by factors such as price increases for the food basket and rising labor costs. At the store level, price hikes boosted revenue streams while simultaneously imposing higher costs (e.g., increased raw material and labor expenses), thereby compressing gross profit margins. The divergent trends in gross profit margins across the two business segments underscore the need for more refined management in structural adjustments.

Meanwhile, the gross profit margin for the supply chain (i.e., the company's provision of raw materials/ingredients and auxiliary supplies to stores) increased by 0.7 percentage points year-on-year, as improved procurement efficiency partially offset cost pressures.

The pressure on gross profit margins at company-owned stores is a potential concern. Should the upward trend in costs persist, it could weaken the profitability of individual stores. The company must strike a balance between supply chain efficiency, operational leverage, and cost control.

Operating profit (business profit) grew robustly, but net profit was dragged down by non-recurring items.

Diluted EPS stood at $4.08, marking a slight 2.6% year-over-year decline but exceeding the market consensus of $3.97. This performance was underpinned by a 12.2% increase in operating income (to $223.2 million), driven by growth in franchise fees and supply chain gross margin expansion, despite a 5.2% year-over-year decrease in net income due to unrealized losses from DPC Dash investments. This beat underscores cost control capabilities. Business shifts include a net store increase of 214 locations (29 in the U.S., 185 internationally), signaling a strategic pivot toward international expansion.

Q3 operating profit increased by $24.3 million year-over-year, representing a 12.2% growth. Excluding currency impacts (currency adjustments in international royalties), the year-over-year growth rate was approximately 11.8%. This growth was primarily driven by revenue expansion, supply chain efficiencies, and increased royalty profits. Operational momentum remains positive, but pressure on net profit highlights the company's sensitivity to non-operating gains and losses. Increased volatility in future investment projects or valuation changes of affiliated companies could pose challenges to the company's earnings stability.

Cash flow from operating activities for the first three quarters reached $550 million, representing a significant improvement over the same period last year. Regarding capital expenditures, the company invested $56.7 million during this period, down from $70.8 million in the prior-year quarter. Consequently, the company's free cash flow (Operating CF – CapEx) for the first three quarters amounted to $496 million, a notable increase from $376 million in the same period last year.

Strong cash flow and prudent capital expenditure management provide a solid buffer for the company to navigate uncertainties while also supporting its ability to reward shareholders.

Same-store sales, store growth, and channel factors are strong in the U.S., while international markets are lagging.

U.S. same-store sales rose 5.2% year-over-year, exceeding most market expectations; international same-store sales increased by only 1.7% year-over-year (below the market consensus forecast of ~1.9%), indicating challenges in international markets.

In terms of store expansion, the company closed some stores during the reporting period while simultaneously opening new stores globally. Store closures were primarily concentrated in underperforming international markets, indicating that the company is undertaking structural optimization in its international footprint.

At the channel level, the company has been proactive in promotions and product innovation—such as relaunching the "Best Deal Ever" promotion and introducing the Parmesan Stuffed Crust—strategies that have driven growth in the U.S. Its distribution channel strategy, including partnerships like DoorDash, is also seen as a key driver of sales growth.

Management Guidance and Market Expectations: Cautious Optimism Prevails

The market widely expects the company's same-store sales to maintain mid-to-high single-digit year-over-year growth in the coming quarters, with the U.S. segment poised to continue leading the way. Ahead of the Q3 earnings release, analysts note that promotions, new product launches, and channel expansion will remain key drivers, though profit margins may face pressure. During the Q2 earnings call, management highlighted that DoorDash expansion, promotional initiatives, and the Rewards program upgrade will positively impact the second half of the year.

Valuation Perspective

Valuation: Domino's current market capitalization implies an estimated 2025 price-to-earnings (PE) ratio of approximately 25 times, pricing in a long-term growth expectation of 3-5%. This valuation is relatively reasonable but not overly generous.

Considering its EPS outperformance and store growth, the market may be underestimating the expansion potential of Domino's supply chain gross margins. Compared to peers like $Papa John's(PZZA)$ (trading at a PE of around 20x but with only 2% same-store growth) or $Yum(YUM)$ (Pizza Hut's parent company, trading at a PE of 28x with broader global expansion), Domino's valuation sits at the midpoint. Its competitive advantage lies in its higher U.S. market share (accounting for approximately one-third of pizza delivery).

However, if the macro slowdown intensifies, valuations may face compression; conversely, increased contributions from aggregators could catalyze a revaluation, similar to $Expedia(EXPE)$ 's path of boosting its valuation through partner collaborations.

Positive Factors: The company continues to drive innovation in products (e.g., Parmesan Stuffed Crust), promotional strategies (Best Deal Ever), and channel expansion ( $DoorDash, Inc.(DASH)$ partnership), providing stronger support for growth. The robust performance in the U.S. market remains the primary growth engine.

Potential Risks: Gross profit margins at company-owned stores face pressure, and their profitability may be constrained until rising food and labor costs ease; sluggish growth in international markets, exchange rate fluctuations, or deteriorating macroeconomic conditions could dampen the performance of the international segment;

Based on current EPS and earnings projections, Domino's valuation already carries a premium (reflecting the market's assumption of higher growth). Assuming a "healthy volume-price structure + robust cash flow + strong resilience in the U.S. market," the risk-reward ratio remains attractive if the company can sustain steady profit returns over the next few quarters. However, caution is warranted regarding the potential impact of rising costs and external shocks on profitability.

Our view is that if the company can maintain cost control, optimize its international store portfolio, and sustain sales growth through promotions and innovation in the next phase, its performance is expected to continue improving steadily. However, if cost pressures intensify further or the international environment deteriorates, its profitability may experience fluctuations. For investors, a "neutral-to-optimistic" allocation bias can be considered based on the company's operational stability and market share advantage when valuations are appropriate.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Venus Reade·2025-10-16DPZ blew right past earnings estimates. Congratulations investors. Still the best stock I've ever owned and have owned it for almost 20 years.LikeReport

- DaveLewis·2025-10-15Great insights on Domino's performance! [Wow]LikeReport

- Enid Bertha·2025-10-16Great earnings! Go DPZ!LikeReport