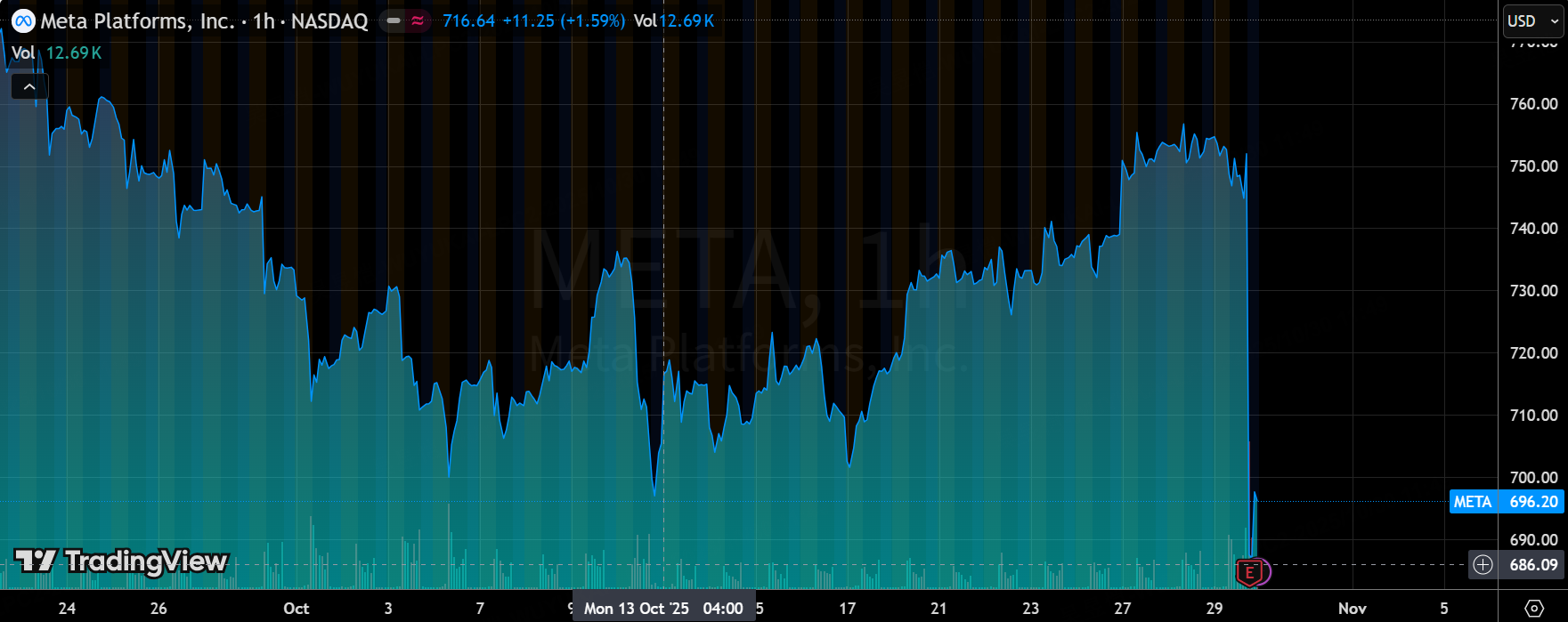

Meta's Dilemma: AI Goldmine Today, But Tomorrow's Gamble Turns -8% Plunge!

$Meta Platforms, Inc.(META)$ Q3 earnings report and the market's reaction to it can be summed up in this sentence:

The good news is that it's finally no longer undervalued (P/E ratio has rebounded).

The bad news is, it may not be achieved through rising stock prices.

Q3 revenue surged by 26%, demonstrating robust growth with the core advertising business continuing to strengthen. However, net profit suffered a significant decline due to a one-time tax impact, plunging by 83% for the quarter. Focusing solely on EPS would show a sharp rise in the P/E ratio. Yet even when considering adjusted EPS, the implied growth rate still raises market concerns about "transitional pains" stemming from structural factors like cost expenditures and capital spending. The subsequent 8% post-market decline thus reflects concentrated market sentiment.

Key Financial Highlights

Revenue Metrics. Total revenue reached $5.124 billion, exceeding market consensus ($4.936 billion), up 26% year-over-year (25% at constant currency), and up 8% quarter-over-quarter (from $4.752 billion in Q2); Key drivers included advertising business growth fueled by AI-optimized recommendation systems, with ad impressions rising 14% and average ad prices increasing 10%. Structural shifts indicate the Family of Apps contributed 99% of revenue, while Reality Labs—though smaller—saw 74% year-over-year growth, suggesting AI hardware (e.g., glasses) is beginning to drive incremental revenue, though core advertising remains the primary engine.

Profit Metrics. EPS: $1.05, down 83% YoY and 82% QoQ; Adjusted EPS (excluding taxes): $7.25, up 20% YoY. The underlying logic is that a one-time non-cash tax expense of $1.593 billion (resulting from the U.S. tax reform) led to reported net income of only $271 million, while adjusted net income reached $1.864 billion. Operating profit reached approximately $2.05 billion, up 18% YoY (below revenue growth rate). The operating margin was approximately 40% (compared to about 43% in Q3 2024). While the operating margin remains healthy, the decline from 43% to 40% indicates a slight decrease in profit elasticity. The business structure highlights how AI investments (such as R&D expenses up 35%) are eroding profit margins. However, the fact of a "sharp drop in net profit for the period" is difficult for investors to overlook.

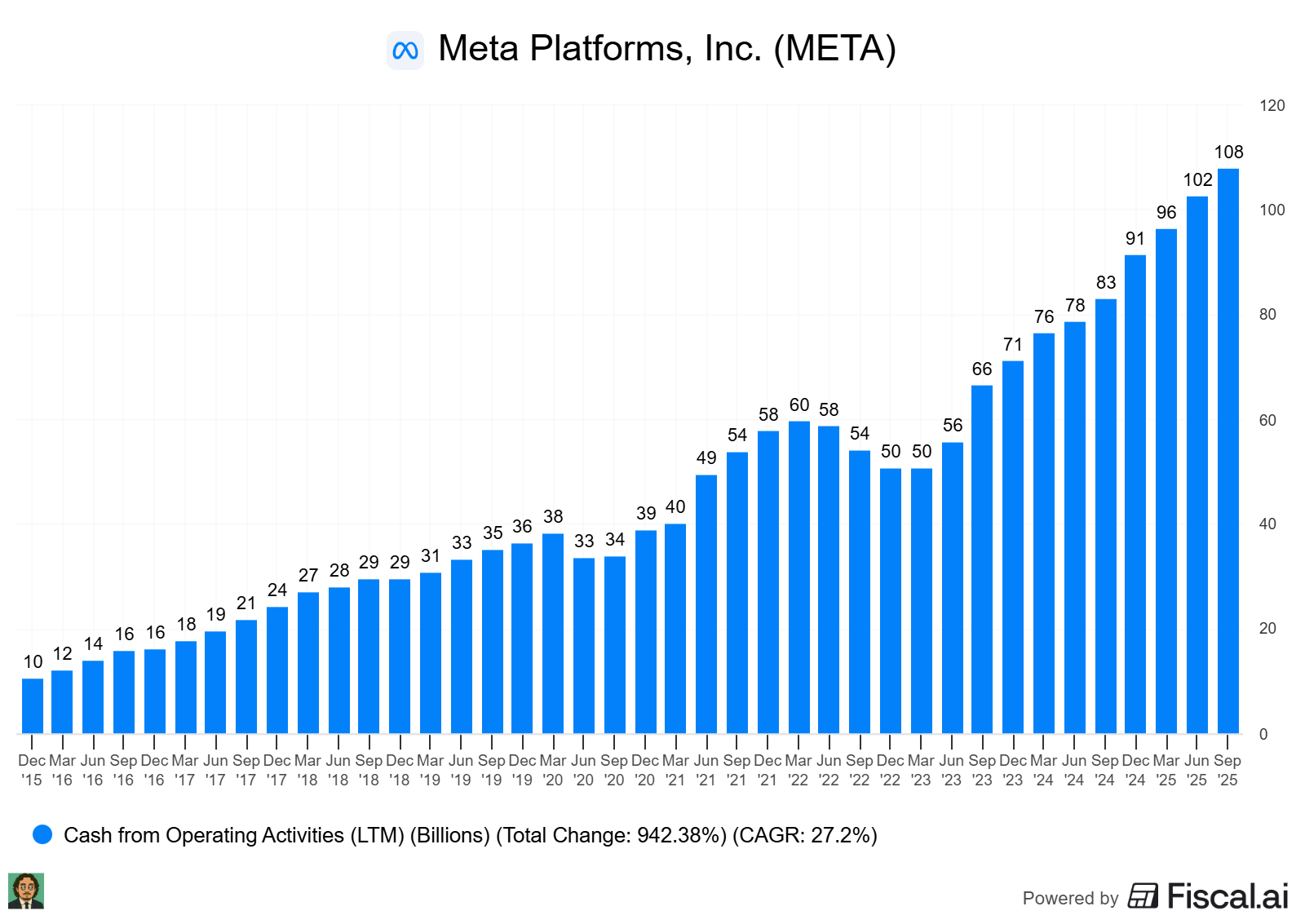

Costs, Capital Expenditures, and Investment Pace. Total expenses for the quarter were approximately $3.07 billion, up about 32% year-over-year (exceeding revenue growth). Quarterly CapEx reached $19.4 billion, up 50% year-over-year, driven by AI infrastructure expansion. This exceeded expectations (full-year guidance raised to $70-72 billion), signaling a shift in investment focus from advertising optimization to cutting-edge AI. This transition is reflected in rising costs and capital expenditures. While strategically sound in the long term, it will exert near-term pressure on cash flow and profit margins.

User and operational metrics. Daily Active Users (DAU) reached 3.54 billion, up 8% year-over-year; Instagram MAU surpassed 3 billion, while Threads DAU exceeded 150 million. Key drivers included AI-enhanced content recommendations (e.g., +30% video watch time) and steady month-over-month growth. Overall results exceeded expectations (market consensus estimated DAU around 3.45 billion), with emerging products like Threads showing signs of transitioning from momentum-driven growth to sustainable expansion.

Q4 revenue guidance is $56.0 billion to $59.0 billion. Management also noted that due to tax law changes, the company expects a significant reduction in its U.S. federal cash tax burden. Despite high one-time tax charges, the future cash tax burden is expected to improve. Full-year expenses are projected at $116.0 billion to $118.0 billion, with emphasis on the "significant acceleration" of CapEx and expense growth in 2026 to support AI infrastructure and model development.

Key Investment Considerations

1. Advertising remains the company's most robust moat and cash flow source. Its reliance on AI recommendation system optimization has proven capable of driving 26% revenue growth, demonstrating greater stability compared to previous quarters (such as the 18% growth in Q3 2024). In other words, even amid fluctuations in other businesses over the short to medium term, the stability of the advertising ecosystem provides core support for the company's cash flow and profitability, serving as a crucial buffer against risks associated with "high investments causing short-term profit volatility." From an investment perspective, the sustainability of advertising should be viewed as part of the valuation's margin of safety, rather than pricing the company solely based on future projections of AI investments.

2. No clear leveraged bets at present. Management has centered its core strategy on AI infrastructure and open-source models (such as Llama), pursuing a "platformization" transformation through establishing a Super Intelligence Lab and front-loading computational investments. This transformation path holds immense long-term value (similar to Amazon's expansion from e-commerce to cloud services), potentially evolving the company from a traffic-and-advertising platform into a broader AI ecosystem. However, two points warrant emphasis: First, this represents a shift from "monetizing traffic" to "monetizing capabilities," with returns likely materializing slowly. Second, inadequate cost management could erode shareholder returns in the short term and amplify valuation volatility. Naturally, recent "off-balance-sheet financing" also raises investor concerns about hidden leverage risks (which have partially reflected in the stock price).

3. Investors focus on return rates. Accelerated CapEx and Opex will become the dominant variables shaping earnings momentum over the next few quarters. The 2025 CapEx floor has been raised by RMB 4 billion to RMB 700–720 billion. Q4 CapEx is expected to increase from RMB 19.4 billion in Q3 to around RMB 20 billion, with the company indicating a "significant upward revision" to its 2026 CapEx forecast. Annual spending is projected at RMB 116–118 billion. Based on the midpoint estimate, Q4 spending will increase by approximately 37%, significantly squeezing the company's cash flow and operating profit. This indicates that revenue growth is notably slower than the pace of returns, creating a "period of input-output mismatch." The monetization pace of CapEx/depreciation and amortization, along with return on invested capital (ROIC, incremental revenue/new CapEx), are key indicators for assessing whether medium-to-long-term returns can be realized.

4. Valuation pressures have emerged. Valuation multiples now demand high certainty regarding growth realization. The current market capitalization stands at approximately $1.89 trillion, corresponding to an adjusted EPS of $7.25 and an implied forward P/E ratio of 26x. Given significantly increased capital expenditures and slowing near-term revenue growth, such valuations require the assumption that "revenue accelerates by 2026 or AI investments rapidly deliver returns." Should 2026 revenue growth fail to accelerate while CapEx/Opex continues rising, adjusted EPS could retreat to the "low double-digit or high single-digit growth" range, exposing the current valuation to downside risks. If the company maintains its current investment pace, short-term profit elasticity will be compressed, eroding shareholder return potential (dividends/buybacks/free cash flow) and undermining the stability of valuation benchmarks.

5. The Core Divergence Between Optimistic and Pessimistic Scenarios: The Pace of AI Returns vs. The Pace of Cost Inflation

Optimistic Scenario (Catalyst): As AI investment begins to translate into product monetization (e.g., new revenue streams like Reels, AI-driven ads, and Reels ARR), it will drive exceptional advertising growth and new service revenues. This will support continued valuation expansion, potentially advancing toward a ~28x valuation multiple with approximately 30% upside potential for the stock price.

Pessimistic Scenario (Risk): If AI investments monetize slower than anticipated while CapEx/Opex has already significantly increased, profits will be diluted and valuations will need to correct downward (similar to the profit pressure Tesla faced during its autonomous driving investment phase or Meta's "lower-than-expected returns after investment" during the 2022 metaverse downturn). This would result in a valuation retreating below 20x.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Enid Bertha·2025-10-31I was waiting and waiting to find a good price to buy in, looks like Christmas came early!LikeReport

- Venus Reade·2025-10-31I was waiting and waiting to find a good price to buy in, looks like Christmas came early!LikeReport

- a9032·2025-10-30It's a tricky situation for Meta.1Report