Google Search Isn't Dead. It's Supercharged (By $91B Capex Bomb)

$Alphabet(GOOG)$ Google delivered its first-ever quarterly revenue exceeding $100 billion in Q1 2025. Both investor focus and management priorities centered on AI returns. First, "AI has begun delivering tangible commercial returns across multiple business lines." Second, to support this surge in demand, significant expansion of AI infrastructure and data center investments is underway (CapEx raised to $91–93B, with projections indicating even higher levels by 2026). $Alphabet(GOOGL)$

Key Financial Highlights

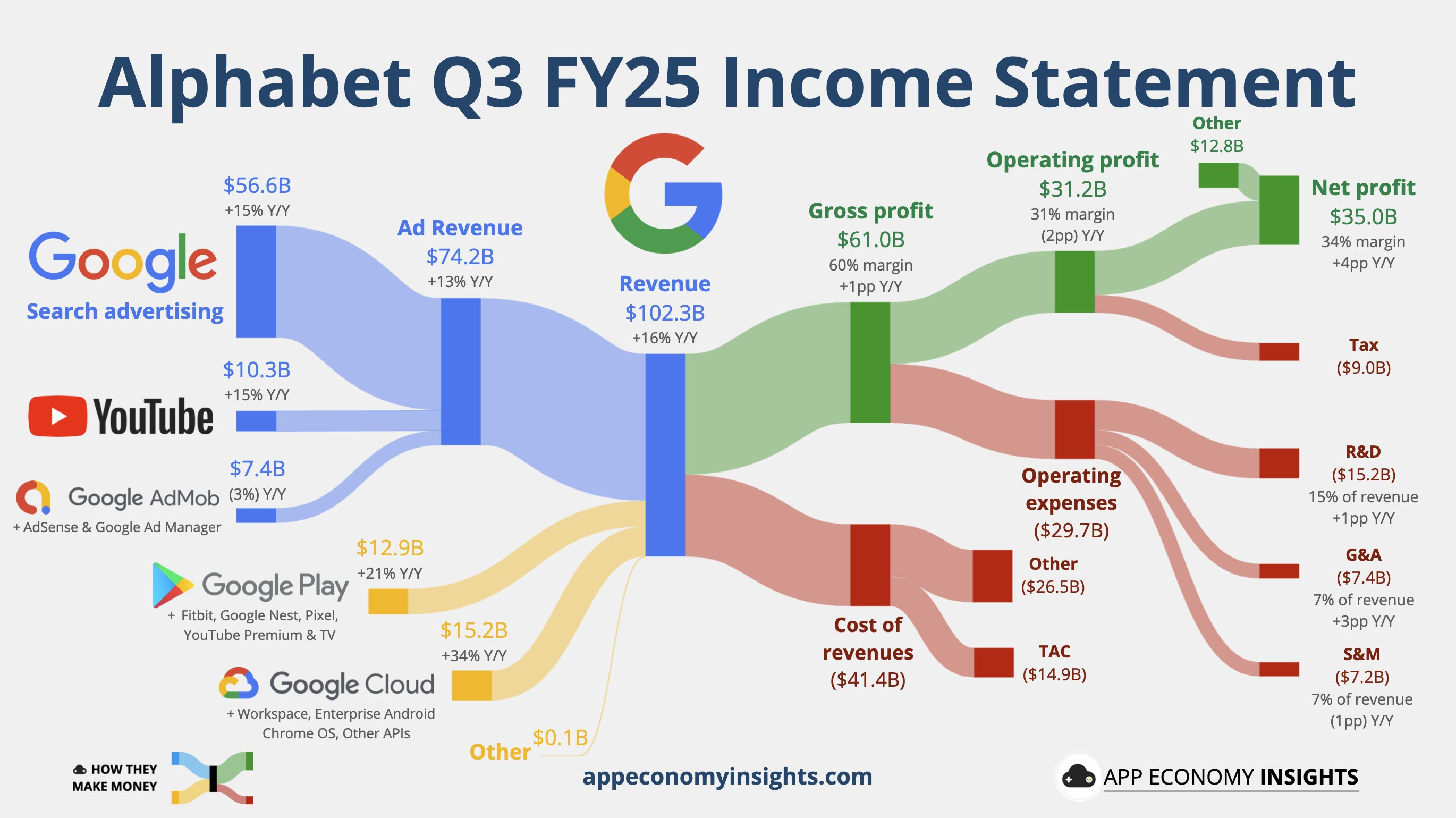

Total revenue reached $102.3 billion, exceeding the market consensus estimate of $99.85 billion. This represents a year-over-year increase of 16% (15% at constant currency) and a quarter-over-quarter increase of 5%. The company's diversified revenue structure is progressively delivering value. Notably, Google Cloud revenue reached $15.2 billion, up 34% year-over-year—marking its fastest growth in recent years. This acceleration was driven by robust demand for AI infrastructure and generative AI solutions. Cloud backlog surged to $155 billion, exceeding market consensus of $148 billion, while core cloud growth further accelerated with customer signings increasing at a 34% faster pace.

Search revenue reached $56.6 billion, up 14.5% year-over-year, also significantly exceeding expectations (some pessimistic buyers even anticipated negative growth). As the company's cash cow, the search business benefited from AI-enhanced query experiences and advertising optimization exceeding expectations. The underlying logic lies in the integration of the Gemini model, which has boosted user stickiness. YouTube advertising revenue also surpassed $10 billion, reaching $10.3 billion, a year-over-year increase of 15%. This growth stems from the popularity of short videos and live content, as well as iterations to AI recommendation algorithms, slightly exceeding market expectations.

Profitability also exceeded expectations. Excluding the EU fine, the operating margin reached 33.9%, indicating that the impact of capital expenditures remains negligible for now and cost control is effective. Although short-term profit pressure persists, the company stands out as exceptionally strong when compared to peers. Earnings per share (EPS) reached $2.87, a 35% year-over-year increase. This leap was driven by a 33% rise in net revenue (to $35 billion), significantly surpassing market expectations of $2.33.

Key Investment Considerations

This quarter, management repeatedly emphasized that "AI is driving tangible business results." This is reflected both in the surface metrics of revenue and user numbers (revenue +16%, search +14.6%, Gemini monthly active users at 650 million, query volume tripled quarter-over-quarter) and in the significant jump in Cloud revenue and backlog (Cloud +34%, backlog +46% to $155 billion).

The entire chain of logic

AI Capabilities (Deeper Answering, AI Overviews, AI Mode) → Increased User Engagement and Query Volume → New Query Types Drive "Net New Queries" (Philipp Schindler's Metric) → Amplified Advertising/Search and Subscription/Cloud Revenue Scale.

With high user engagement, Gemini's monetization path is becoming increasingly clear. Management disclosed Gemini's monthly active users at 650 million, with query volume growing 3x from Q2 to Q3. AI Overviews are cited as the core product "driving net new queries." AI Max is the "fastest-growing AI search advertising product," generating billions of net new queries in Q3. Gemini isn't merely replacing queries; it's extending demand for longer-form, multi-round, and multimodal interactions (e.g., longer queries in AI Mode). This benefits user stickiness and ecosystem penetration (YouTube, Maps, Ads, Cloud).

If the AI format can expand the query base without significantly reducing the effective CPM (eCPM), advertisers will gain long-term benefits. Conversely, if long queries replace high-eCPM short queries, there is a risk of declining monetization efficiency.

Cloud backlog surges alongside soaring enterprise demand. Cloud backlog has grown to $155 billion (a 46% quarter-over-quarter increase, adding $49 billion), directly reflecting robust demand. This rapid expansion of backlog reduces short-term unpredictability, but requires monitoring of contract term structures, cancellation clauses, and gross margin levels.

Capital expenditures (CapEx) have been significantly increased to support long-term AI/Cloud investments, though this will temporarily weigh on the horizontal income statement. CapEx guidance has been raised from $85 billion to $91–93 billion (2025), with a "substantial increase" anticipated in 2026. Management also emphasized the deployment of in-house TPU and NVIDIA GPU (A4X Max / GB300) in data centers.

Additionally, regarding agentic e-commerce and Waymo, management views these as long-term opportunities, highlighting Waymo's expansion potential in 2026 and the scope for integration with the in-vehicle Gemini system. Key risks include uncertainty around monetization rates for new AI queries, upward pressure from depreciation and energy consumption due to capital expenditures, cloud pricing competition and customer bargaining power, as well as macroeconomic/currency fluctuations (the company has noted potential FX tailwinds or volatility in Q4).

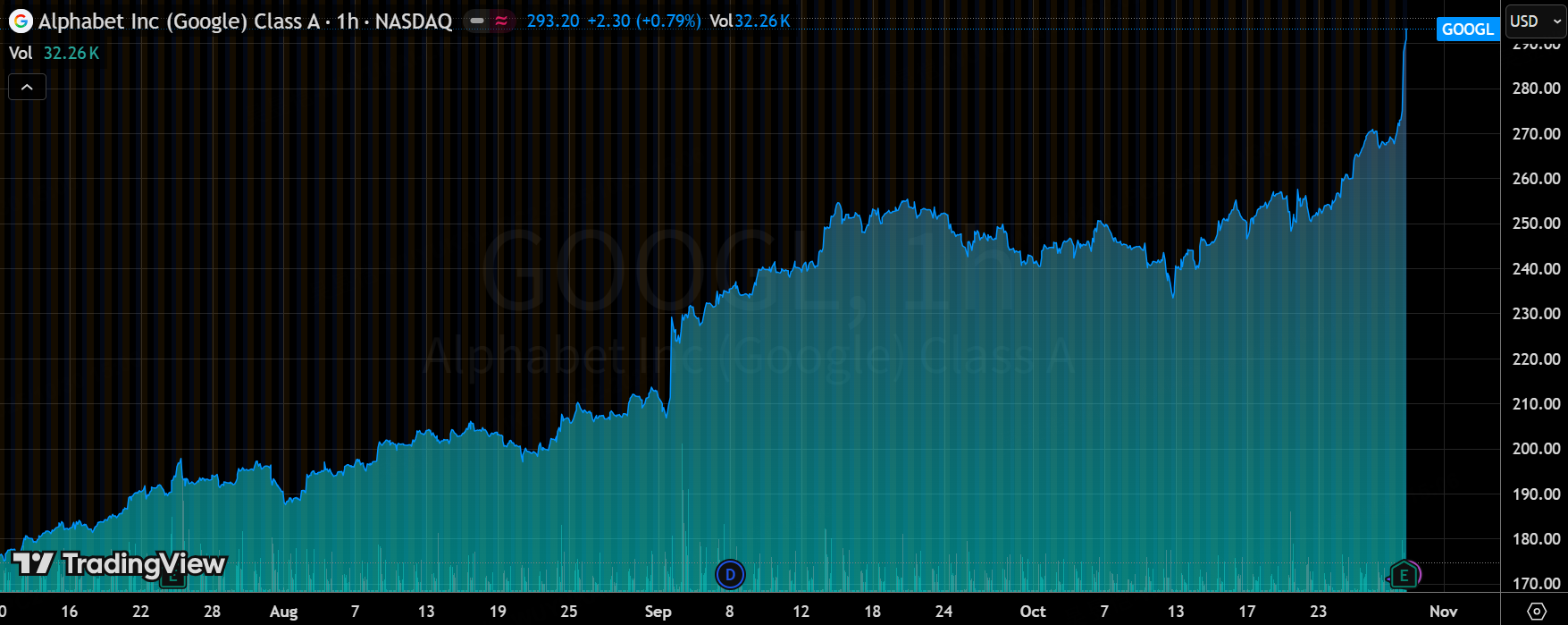

From a valuation perspective, the current post-market-close price-to-earnings ratio stands at approximately 28 times. Based on the current 2026 guidance and market expectations, this implies an annualized growth forecast exceeding 20%. However, profit margins remain highly uncertain amid significant capital expenditure. Consequently, the current market pricing is moderate and slightly above the five-year average.

The 14.5% growth rate in its search business fell below historical peaks, potentially underestimating the long-term multiplier effect of AI integration; Compared to peers, Alphabet's cloud growth (34%) trails Microsoft Azure's 40%, yet commands a lower valuation (EV/EBITDA ~20x vs. Microsoft's 25x). This provides investors with a buffer: further cloud penetration could drive valuation expansion, while stagnation may trigger a pullback.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Enid Bertha·2025-10-31TOPIMO Alphabet is the best company of the Mag 7. It had revenues of $102.3B for just one quarter. Alphabet's revenues will be larger than Apple's sometime before the end of next year.LikeReport

- Valerie Archibald·2025-10-31TOPIMO Alphabet is the best company of the Mag 7. It had revenues of $102.3B for just one quarter. Alphabet's revenues will be larger than Apple's sometime before the end of next year.LikeReport

- 0billionaire·2025-10-30Incredible insights! This is a game changer! [Wow]LikeReport